How Can Enterprises Survive in the Fierce Market Competition of the EV Batteries?

- Out of confidence in market recovery and the Ministry of Industry and Information Technology's planning goals for new energy vehicle ownership, the overall development environment for new energy vehicles in 2020 will be good, which will drive the growth of demand for EV batteries.

- With the subsidy declined, the cost difference between lithium iron phosphate batteries and ternary lithium batteries is also more obvious, and lithium iron phosphate batteries are expected to get developed again with its cost advantage. But from a long-term perspective, as energy density is the main theme of the battery, ternary lithium batteries with higher energy density will be further developed in the future.

- Faced with competition, it is necessary and significant for battery companies to build long-term cooperation with downstream OEMs to lock in market share and extend their industrial chain with high-quality products and service.

How Much is EV Battery Demand in China in 2020?

Benefiting from the rapid growth of sales in the new energy vehicle industry, the shipments of EV batteries are rising. As government subsidies will be withdrawn after 2020, and the cost of lithium batteries will continue to decline, the cost-effectiveness of new energy vehicles as consumer products will gradually be reflected, so the demand for EV batteries will increase steadily in the next few years.

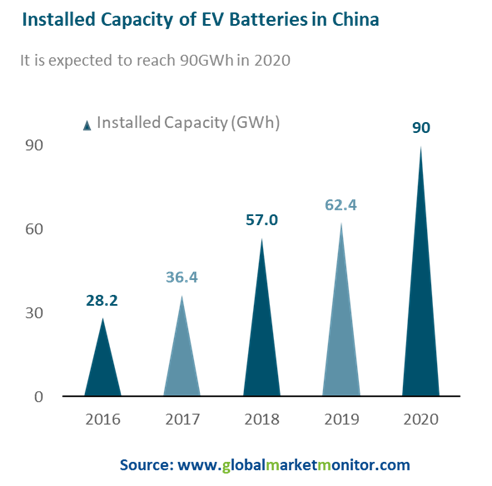

The number of new energy vehicles has a great effect on the demand for EV batteries. According to the planning of the Ministry of Industry and Information Technology, the ownership of the domestic new energy vehicle will reach 5 million by 2020 with the sales of 2 million, accounting for about 12% of the total sales. It is estimated that the demand for EV batteries will reach 90GWh in 2020 based on the average energy consumption of 45kWh.

Market Competition for the Two Leading Domestic EV Battery Leaders

There are two common EV battery routes, mainly including ternary lithium battery technology routes and lithium iron phosphate battery technology routes.

CATL is a major ternary lithium battery manufacturer in EV battery field in China, whose technical route is mainly based on the high-nickel ternary lithium architecture, relying on reducing the number of modules to directly form a standardized battery pack from multiple large-capacity batteries. At the same time, in the case of constant charge and discharge rate, the CTP technology of CATL only needs to adopt a simple series structure to output or accept a larger current, with stronger power and faster charging.

The blade battery of BYD is based on the lithium iron phosphate technology it is good at. The battery cell is also evolving to a large capacity with a smaller battery cell. It is estimated that the energy density of the blade battery can reach about 180Wh/kg.

Lithium iron phosphate battery has the characteristics of safety, stability, and low cost, which has been used as a new energy vehicle EV battery in the early days. Later, as new energy vehicle subsidies increasingly required battery energy density and other indicators, ternary lithium batteries gradually became the mainstream in the EV battery market due to their advantages in cycle life and endurance.

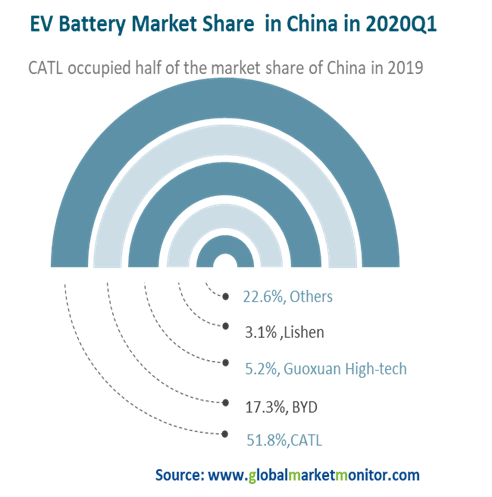

Data show that in 2019, the share of installed capacity of lithium iron phosphate batteries is 32%, and that of ternary lithium batteries is 62%. Among the installed capacity of EV batteries in China in 2019, CATL occupied 51% of the whole share, and BYD of 17.3% and Guoxuan High-tech of 5.2%.

The Public Is More Sensitive to the Cost of Electric Vehicles After the Subsidies Declined

In April of this year, the State Council's comprehensive technological progress, scale effect, and other factors extended the implementation period of the new energy vehicle promotion and application of financial subsidy policy to the end of 2022. To ease the intensity and rhythm of subsidy withdrawal, in principle, the subsidy standards for 2020-2022 will be 10%, 20%, and 30% on the basis of the previous year. The subsidy policy has gradually receded, and the market is more sensitive to the cost of electric vehicles. At the same time, the expectation of the performance of automobiles has continued to increase, making the market increasingly fierce, and the industry pattern has gradually concentrated in the industry.

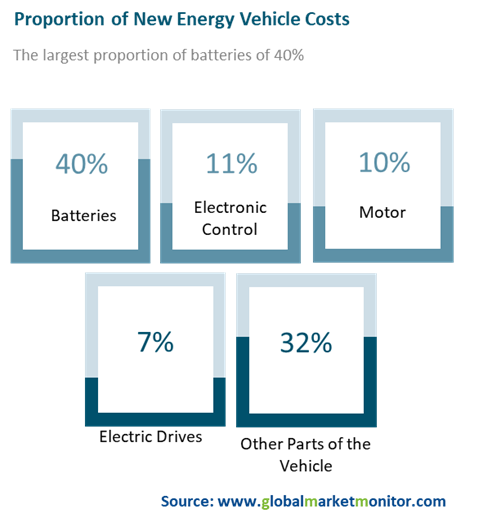

The EV battery is the core of the new energy electric vehicle, which accounts for up to 30% to 40% of the total vehicle cost, which directly affects the battery life and safety of the electric vehicle. Therefore, the EV battery determines the development level and direction of new energy vehicles. Whoever has the EV battery will have the pricing power and industrial initiative of the electric vehicle.

As the trend of subsidy retreat or even cancellation of new energy vehicle cost reduction will be more obvious, the cost difference between lithium iron phosphate battery and ternary lithium battery will be more obvious. The lithium iron phosphate battery is expected to get developed again due to its cost advantage. The use of lithium iron phosphate batteries is an important means for many auto companies to respond to the subsidy retreat and achieve a rapid reduction in the cost of electric vehicles.

Cooperation with Car Companies to Lock in Market Share Is the Basis for Long-Term Survival

As the world's largest new energy vehicle market, China has become the main battlefield for many foreign EV battery companies. A large number of foreign EV battery companies headed by Japan and South Korea have entered the Chinese market, with the total investment of LG Chem, Panasonic, and Samsung in China reaching as high as 57 billion yuan.

In the past, subject to the restrictions of the national subsidy policy, foreign-funded batteries were not subsidized in the domestic loading of vehicles, which led to foreign batteries failing to enter the mainstream market. After policy subsidies receded, real market competition began.

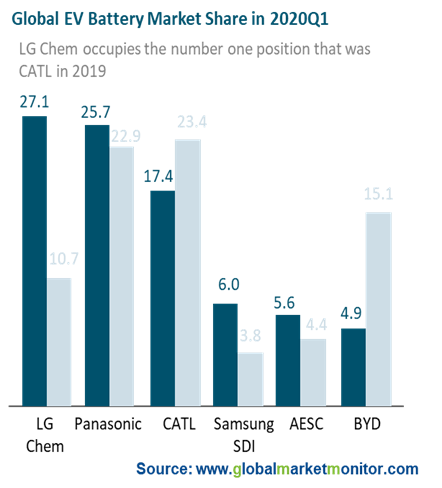

According to data of the first quarter of 2020, the market share of LG Chem has more than doubled from the same period in 2019, occupying the top position; CATL won the third with the market share of 17.4%.

In the case of increasingly fierce competition in the domestic EV battery market, the price war is only an expedient measure to gain share in the short term. Thus, it is necessary and significant for battery companies to build long-term cooperation with downstream OEMs to lock in market share and extend their industrial chain with high-quality products and service.

The lithium battery industry chain is gradually transitioning from Japan, and South Korea to China, and the supporting industry chains of China, Japan and South Korea are also increasingly optimized; in particular, the comprehensive competitiveness of China is highlighted, which is expected to lead the global electric vehicle into a true parity era. In the short to medium term, the global competitive landscape of EV batteries will be dominated by LG Chem and CATL.

LEARN MORE:

Hydrongen Fuel Cells

https://www.chinamarketmonitor.com/reports/372846-hydrogen-fuel-cells-market-report.html

Lithium-ion Batteried for Automotive